Dedicated to Credit Union Innovation

Delivering innovative technology solutions to help credit unions achieve more.

Analytics

Access insights into members, consumers, and operations all in one powerful platform.

Cloud

Scale your credit union with secure cloud services from our team of experts.

Talent

Get access to specialized talent for all your credit union tech/data staffing needs.

Solving a diverse set of challenges for credit unions of all sizes for over 30 years.

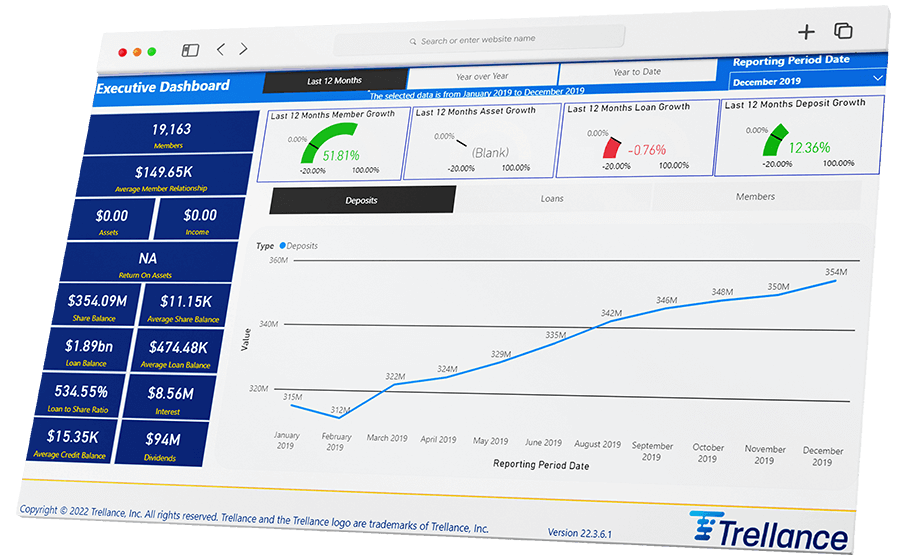

ANALYTICS

Data-Driven Insights to Improve Member Experience

Our suite of advanced analytics solutions can help your credit union achieve excellence in member experience and portfolio growth. Learn more about your members and secure an improved understanding of your business performance through powerful data visualizations.

CLOUD

Achieve More With Your Credit Union

Secure, streamline, and scale your credit union with Trellance Cloud and the support of our team of credit union IT experts. Best-in-class cloud platforms, both public and community, with currently over 1,000 servers and 5,000 end points managed at hundreds of credit unions.

TALENT

Get the Talent You Need as Soon as Tomorrow

Get the tech talent you need when you need them and stop sitting stagnant while trying to fill positions. Our talent team can help with data analytics, software development, testing, infrastructure support, and more.

The Trellance Difference

About us

Why Choose Us?

Credit Union Expertise

We understand the complexity of meeting the ever-evolving expectations of the modern digital member.

Dedicated to Data Quality

Our solutions are designed for rapid deployment, fast ROI and reduced TCO by leveraging the benefit and scale of modern cloud technologies.

Simplify Complexity

Our experts understand the IT systems used by credit unions and know how to integrate disparate ecosystems.